Water Is No Longer Overlooked — It’s Becoming Essential

For years, water has been one of the most underappreciated sectors in global markets.

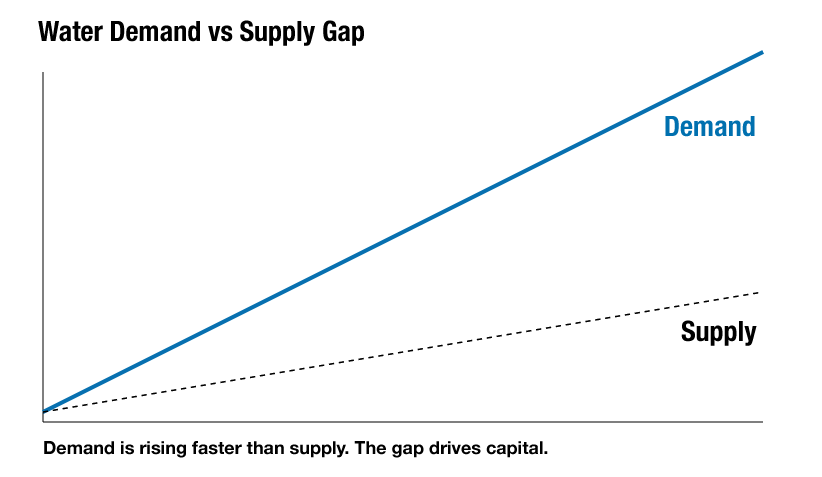

Over the past 12–24 months, water has begun to shift from a background infrastructure issue to a front-line economic priority. Not because of hype, but because of reality.

Demand is rising. Supply is constrained. Infrastructure is aging. Regulation is tightening.

And capital is starting to follow.

The Conditions That Drive Investment Cycles

The most successful investment sectors tend to share a few characteristics:

- Demand is non-discretionary

- Infrastructure is underbuilt

- Spending is mandated or regulated

- Capital arrives late—but then accelerates

Water now checks every one of those boxes.

This is not theoretical. It’s structural.

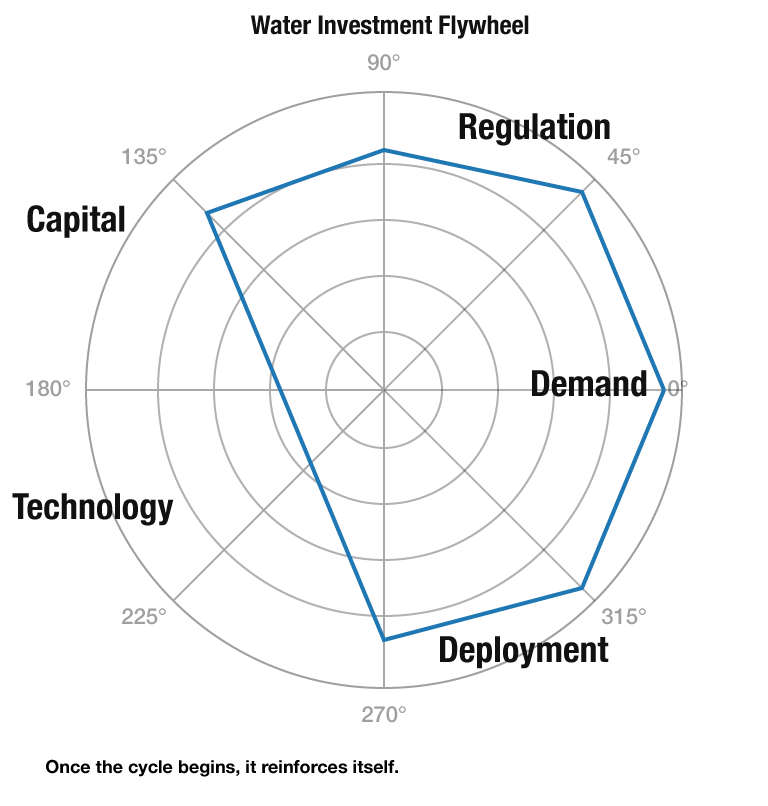

Industrial users need it to operate. Municipalities are required to provide it. Governments are investing heavily to secure it. And climate pressure is making delays increasingly costly.

When those forces converge, investment cycles form—and they tend to last for decades.

Recent data points make this clear:

- Over $1B annually is flowing into water technology investments

- The European Investment Bank committed €15B to water-related initiatives in 2025

- Institutional investors are increasing allocations to water infrastructure and treatment technologies

- Venture funding in water tech has reached or approached record levels

Major organizations—from global consulting firms to financial institutions—are now describing water as a long-term structural investment theme.

This is not early speculation.

This is early confirmation.

Why Water Is Different From Other Sectors

Water has a unique investment profile:

- It is non-cyclical — demand does not fall in downturns

- It is regulated — spending is often required, not optional

- It is local and physical — meaning infrastructure must be built and maintained

- It is globally constrained — scarcity is increasing

Very few sectors combine all of these characteristics.

Even fewer are still early enough in their capital cycle to offer asymmetric upside.

The Technology Inflection Point

Historically, water has lagged other industries in innovation due to:

- Long adoption cycles

- Conservative buyers

- High reliability requirements

That phase is ending.

New technologies are now:

Proven at pilot scale

Demonstrating clear ROI

Moving into early commercial deployment

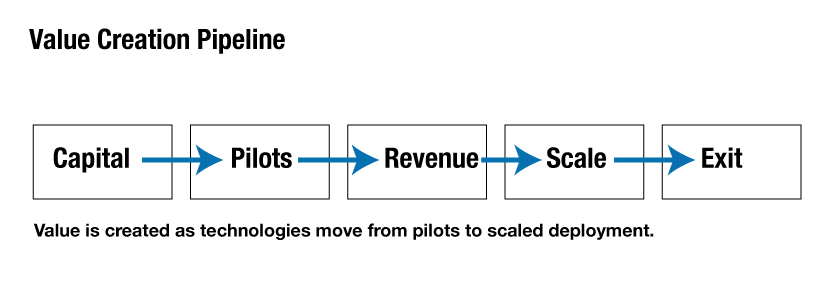

As a result, the sector is transitioning from:

Validation → Deployment → Scale

That transition is where value is created.

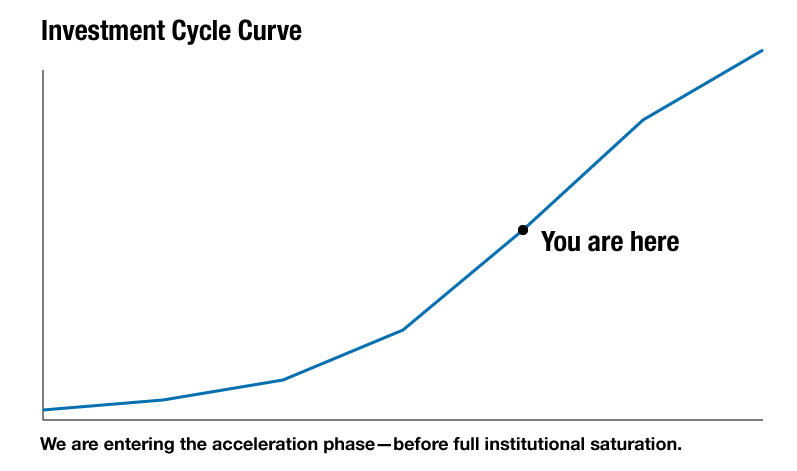

The Window for Early Positioning

In infrastructure-driven sectors, timing matters.

Early capital:

- Enters before institutional saturation

- Benefits from valuation expansion

- Aligns with strategic acquisition demand

Later capital:

- Pays higher prices

- Accepts lower upside

- Competes for access

The water sector is now moving through that transition point.

Where IX Water Fits

At IX Water, we have spent years doing the hard part:

Developing and protecting core technology

Engineering full-scale systems

Validating performance in real-world conditions

Positioning for industrial deployment

While much of the market is just beginning to recognize the opportunity, we are already aligned with it.

That positioning matters.

Because when capital accelerates into a sector, it does not fund ideas—it funds readiness.

Water is no longer an overlooked infrastructure category.

It is becoming one of the most important—and investable—sectors in the global economy.

The shift is underway.

Capital is moving.

Adoption is accelerating.

The only real question is timing.

The opportunity is not in recognizing the trend — It is in positioning ahead of it!

Portions copyright 2026, Hayduke Environmental Consulting. Used with permission.

Top 12 Recent Articles Supporting Water Investment

1.“Rising Tide: Growth Projections for Water Investment” (2025)

👉 Massive capital is already flowing into water, with many organizations investing $500M+ annually, signaling institutional conviction.

2. “3 Trends Defining Water Innovation in 2025” – World Economic Forum (2025)

👉 Water is becoming core to global business strategy and climate resilience, not optional infrastructure.

3. “Investing in Water Tech: Why Now and Where to Focus” (2025)

👉 Huge supply-demand gap + underinvestment creates a once-in-a-generation opportunity in water tech.

4. “Is Water Investment Set to Surge?” – Roland Berger / White & Case (2025)

👉 Describes a “rising tide of capital” and a historic opportunity for investors in water infrastructure and tech.

5. “Water Tech 2025: Innovation Meets Urgency” (2026)

👉 Venture investment remains near record highs, showing sustained investor confidence in the sector.

6. “WaterTech Funding Trends 2025” (2025)

👉 Investors are actively targeting specific high-growth segments in water tech, indicating market maturity and specialization.

7. “WaterTech Challenge: Funded Startups in 2025” (2025)

👉 Water tech funding hit record levels (~$1.12B), driven by scarcity, regulation, and infrastructure demand.

8. “The State of Water Tech Funding 2025” (2025)

👉 Investment has “shattered previous records,” signaling a structural shift in investor appetite.

9. “Breadth and Depth Make Water an Attractive Long-Term Investment” – Robeco (2025)

👉 Water is a stable, long-duration growth theme driven by infrastructure cycles and climate pressure.

10. “The Urgent Case for Water Innovation” (2024–2025)

👉 Returns are becoming increasingly compelling as technologies reach commercial adoption.

11. Reuters: “EIB to Invest €15B in Water Sector” (2025)

👉 Governments are deploying tens of billions and crowding in private capital—classic early signal of a major investment cycle.

12. Wall Street Journal: “Opportunity in U.S. Water Infrastructure” (2025)

👉 Water infrastructure is viewed as resilient, long-term, and less volatile than energy, attracting new dedicated funds.

— IX —

0 Comments